The five new collection suits on six notes, some of them cosigned, were brought

by JAVITCH BLOCK LLC, a law firm with Texas offices located in Richardson, TX that currently

lists four Texas attorneys on its pleadings: Karen Guenther, Jacob M. Figelman,

Elaina Moore, and Marc A. Melamed. Figelman and Melamed are listed on the clerk’s

docketing system as attorneys of records.

The other highly prolific litigator on behalf

of the trusts, MICHAEL J. SCOTT PC / SCOTT PARNELL & ASSOCIATES, has not

filed any new collection actions – at least not in Harris County courts-at-law

-- but has several appeals of National Collegiate student loan judgments pending

in the Houston Courts of Appeals. See page on --> Appellate litigation of National Collegiate Student Loans in Texas.

LOAN DOCUMENTATION ATTACHED TO NCSLT PETITIONS

Little appears to have changed in the

freshly commenced actions, compared to those filed earlier in the year. It is impossible to determine whether any claims are time-barred, or whether they have been vetted with a view to limitations issues. See --> CFPB and enforcement of limitations bar in private student loan debt collection.

Likewise, it is impossible to know what proof of assignment will be produced, if any, upon motion for default or summary judgment, or at trial.

Likewise, it is impossible to know what proof of assignment will be produced, if any, upon motion for default or summary judgment, or at trial.

All five new cases had the Application/Signature Page and the Note Disclosure Statement attached to the initial pleading. None of the attachments, however, included the

terms-and-conditions pages of the loan origination documents. Only one

included an assignment-related document in the form of a Deposit and Sale Agreement for National Collegiate Student Loan Trust 2007-3. Of course, these document are not required at the pleading stage. See more generally ---> Documentation in NCSLT Student Loan Debt Collection Suits

Of the small new batch, only only collection action named two defendants (student borrow

and cosigner) although it was not the only case with a co-signed note. Two lawsuits were against the same borrower, but were filed separately

because they involved two different trusts as Plaintiffs. One of these two,

in turn, comprises claims on two distinct loans made under different loan programs,

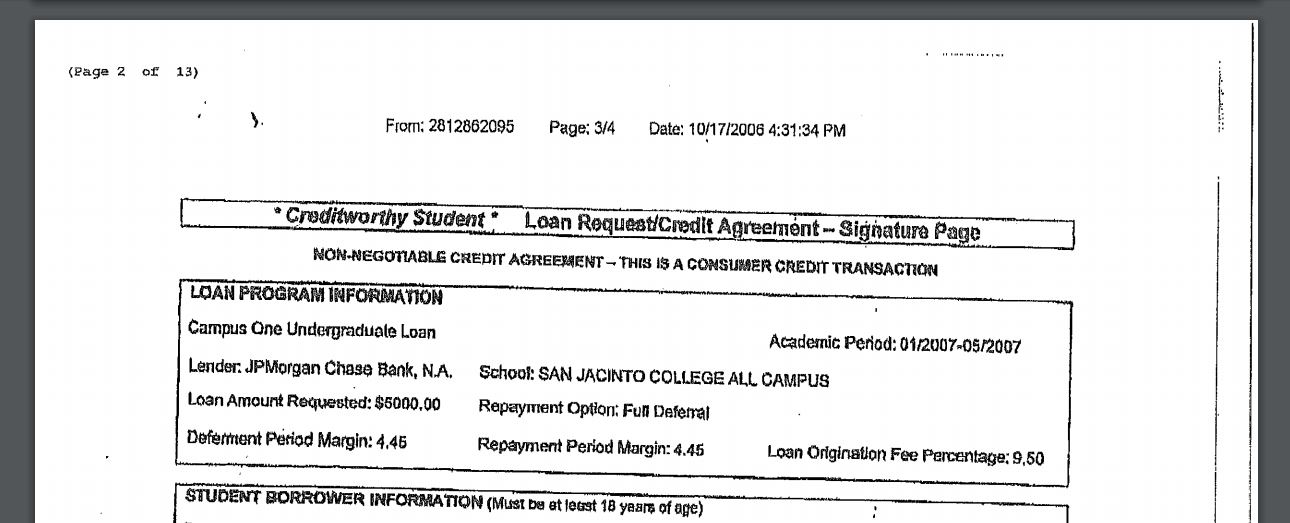

albeit by the same lender: JPMorgan Chase (Campus One Undergraduate Loan and

Education One Education One Undergraduate Loan). Presumably the two loans ended

up in the same securitization transaction. For illustration purposes, images of the entire petition is appended below, following reproductions of the Signature and Note Disclosure Statements from the other cases.

A COMMON THEME: HIGH-COST PRIVATE STUDENT LOANS

A common characteristic of these student

loans, as revealed by the attached documentation is their high cost, and the

deceptive manner in which they were originated, which is apparent on the face

of the documentation attached as exhibits to the pleadings, however sparse.

Compare disclosure of interest rate as "Margin" (above) and as APR

on the TIL Disclosure Statement later (below)

In order to understand the true cost of the loan at the time of application and signing, the applicant would have to know what LIBOR is, and what the LIBOR rate was in effect at the time, and would further have to appreciate that the origination

fee would be added up front to the amount of loan sought, and would also incur interest, along with the amount disbursed.

FAILURE TO MAKE STUDENTS AWARE OF THE TRUE COST OF THE LOAN UP FRONT

FAILURE TO MAKE STUDENTS AWARE OF THE TRUE COST OF THE LOAN UP FRONT

The Note Disclosure Statements in all

cases reflect that all loans were approved for the requested amount (in one case for a higher amount than the pre-printed one on the application), but in each

case the origination fee was even higher -- relative to the disbursed amount --

than the origination fee percentage shown on the application/signature page. And

since the computed origination fee was immediately added to the loan balance as

principal, it also immediately became subject to the accrual of interest at the same high APR. The composite annual cost of the loan (expressed as a percentage of the amount proceeds received) would therefore be more than

the sum of the APR and the Origination Percentage. See "cost index" below, which is the sum of the APR and the nominal origination fee percentage.

| Click on image to enlarge it, or go to bottom of page for larger version |

BELATED DISCLOSURE OF EFFECTIVE APR AND AMOUNT OF ORIGINATION FEE

In each case, the Note Disclosure

Statement that shows the true interest rate, i.e. the APR representing the sum of LIBOR and MARGIN, as

well as the actual dollar amount of the original fee has a date on it that is

at least five days after the date of the signature. So the borrowers could not

have seen them at the time they signed, and would have had to cancel the loan

upon receipt of the disbursement check in order to avoid being on the hook on the much more unfavorable credit-cost terms than those suggested by the application materials.

This assumes that the students even received the Disclosure with

the higher cost-of-credit terms at that time they received the loan disbursement check to allow for the exercise of that option

based on a more complete information about the true cost of the loan they had

applied for. The copy that is submitted in support to the claim in court is the

“LENDER COPY” that contains no evidence on its face that it was mailed to or otherwise shared with the borrower (unlike the Signature Page, that typically contains fax meta data in the header or footer of the page).

EXEMPLARS OF LOAN ORIGINATION DOCUMENTS FROM THE FIVE NEW CASES (FILED ON BEHALF OF STUDENT LOAN TRUSTS FORMED IN 2006 AND 2007)

COMPLETE ORIGINAL PETITION FROM NCSLT COLLECTION SUIT

ON TWO LOANS BY SAME PROGRAM LENDER

("CREDIT-WORTHY STUDENT, ERGO NOT CO-SIGNED)

OVERVIEW OF LOAN ORIGINATION DATA FOR THE NEW CASES

SHOWING COST-OF-CREDIT TERMS AND DELAY IN TIL DISCLOSURES IN DAYS

No comments:

Post a Comment